Hit enter to search or ESC to close

19 October 2022

Insurance Market Update

As the Government moves to increase EQC cover for homeowners, we take a closer look at what this means and whether the change is likely to result in reduced premiums. We also review the impact of climate change and other issues on insurer premiums and discuss the risk of underinsurance in a high-inflation environment.

How EQC changes affect homeowners

The Government is increasing the amount of cover Toka Tū Ake EQC (Earthquake Commission) will provide homeowners in the event of a natural disaster (earthquake, tsunami, volcanic eruption, hydrothermal activity and natural landslip).

From 1 October 2022 the maximum amount of EQC cover will rise from $150,000 to $300,000 plus GST. The new level of cover will apply to all qualifying new or renewing insurance policies that begin on or after 1 October 2022. For policies already in force at 1 October 2022, the new level of cover will not apply until the policy is renewed.

Because EQC is taking on more risk, the annual EQC levy will increase from a maximum of $300 per unit to $480 per unit (plus GST) from 1 October 2022. Where the cover for a dwelling is less than $300,000 then the levy will be charged at 16c per $100 of sum insured.

The changes to the maximum EQC cover and levy amounts apply to residential dwellings, which include houses, individual apartments, rest homes, retirement villages and residential body corporates. To qualify for EQC cover the dwelling must have a fire insurance policy in place.

Government expects change to drive lower premiums

EQC Minister The Hon Dr David Clark has explained the higher EQC cap is to ensure that “private insurance cover remains available and affordable”. He has also stated that as “the Government, through the EQC, will take on a greater portion of risk, I’d expect to see insurers reflect this in their pricing for residential property insurance purchased by New Zealanders after October 2022”.

The Government’s clear expectation that the change will lead to lower premiums highlights a clash between community and risk-based models. Unlike EQC’s community pricing model, in which the price of EQC cover is applied equally across region and construction type, commercial insurance companies use risk-based pricing. This means that the premium they charge reflects the perceived exposure of each individual risk.

As seismic modelling shows that the risk of an earthquake is higher in regions such as Wellington, Hawke’s Bay and Canterbury, the insurance companies charge higher premiums in these areas.

Regional variations: possible scenarios

In the tables below we have explored how these changes could have quite different outcomes for insurance costs depending on where the risk is situated.

The premium charged by insurers for natural disaster insurance in Wellington is significantly higher than in Auckland and so the changes to EQC cover mean the overall price for a policyholder in Wellington could reduce by 14 percent, whereas in Auckland, it may increase by 19 percent. This means policyholders outside high seismic zones need to be prepared for potential increases in overall insurance costs.

|

WELLINGTON DWELLING |

||

|

|

Pre 1 October 2022 |

Post 1 October 2022 |

|

Total replacement cost |

$1,000,000 |

$1,000,000 |

|

EQC Cover |

$150,000 |

$300,000 |

|

Natural disaster cover provided by insurer |

$850,000 |

$700,000 |

|

Typical rate charged by insurance company for natural disaster |

0.65c per $100 of cover |

0.65c per $100 of cover |

|

Insurance company’s premium |

$5,525 |

$4,550 |

|

EQC Levy |

$300 |

$480 |

|

Overall cost to insured |

$5,825 |

$5,030 |

|

AUCKLAND DWELLING |

||

|

|

Pre 1 October 2022 |

Post 1 October 2022 |

|

Total replacement cost |

$1,000,000 |

$1,000,000 |

|

EQC Cover |

$150,000 |

$300,000 |

|

Natural disaster cover provided by insurer |

$850,000 |

$700,000 |

|

Typical rate charged by insurance company for natural disaster |

0.04c per $100 of cover |

0.04c per $100 of cover |

|

Insurance company’s premium |

$340 |

$280 |

|

EQC Levy |

$300 |

$480 |

|

Overall cost to insured |

$640 |

$760 |

(Note: rates used here are indicative of actual rates applied by insurers but will vary from risk to risk).

Accounting for 'all other perils'

As well as applying a natural disaster rate when calculating a premium, insurers also apply a rate to cover ‘all other perils’ such as fire, flood, storms and other weather events. This means policyholders in flood-prone and other high-risk areas may find the rise in their ‘all other perils’ premium outweighs any reduction in their natural disaster premium.

As the EQC changes only affect one component of the insurance premiums (albeit a large one for high seismic areas) the overall effect on insurance costs for dwellings post 1 October 2022 will vary according to the circumstances of individual policyholders.

Is the Wellington insurance market likely to benefit?

There has been much discussion over whether the Government’s move to assume more risk will act to free up Wellington capacity in the commercial insurance market and, if so, will this impact availability and pricing of overall Wellington capacity?

The main insurers in New Zealand have not yet confirmed their stance and we will watch this space with interest as it develops over the next 12-month cycle. However, the impact of inflation driving higher sums insured and increased natural disaster reinsurance costs will most likely be a consideration.

EQC - things to consider

The impact of these changes will vary according to client and region. We recommend discussing the changes with your broker, who can estimate the impact of the changes on the cost of your insurance cover so you are aware of the financial implications.

This information will also assist with budgeting if the cost could be significantly different from the amount you currently pay.

Climate change chills insurers’ bottom lines

Insurers are feeling the combined impact of rising weather-related claims, supply chain constraints and increased costs on their bottom lines. While the two largest insurers in the New Zealand market, Australian-based IAG and Suncorp, both turned in profitable results for the year ended 30 June 2022, their profits were largely driven by premium increases (IAG increased its gross written premium by seven percent and Suncorp by 14 percent). However, the results for both insurers were affected by higher claims for natural catastrophes, including storms.

These two insurers together account for well over 60 percent of the non-life insurance premiums written in New Zealand and for an even larger proportion of the personal lines insurance market. This means the amount of home and contents claims, both here and in Australia, significantly impacts their results, which in turn influences the underwriting strategy for the commercial market.

Climate creating multiple challenges for insurers

Unprecedented changes in global weather patterns and extreme weather events – along with the associated increase in expenses from claims – have made the accurate underwriting of risk substantially more difficult for insurers.

IAG CEO Nick Hawkins said climate change and its impact on customers and communities is one of the most important challenges IAG faces. He commented that “FY22 was one of the most significant peril years we have experienced, with multiple events in Australia and New Zealand.”

Vero NZ CEO Jimmy Higgins voiced similar concerns, saying “Multiple weather events experienced during the year resulted in the highest volume of claims since 2018; and customers experienced longer waiting times for repairs to their homes and vehicles because of the delay in getting materials.”

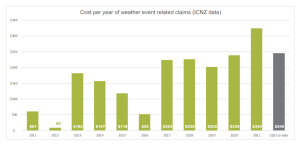

In New Zealand, extreme weather claims have nearly reached $200 million for the year to 30 June 2022, closing in on last year’s record payment of $324 million. These figures are set to jump, with claims from three July storms totalling $43.7 million alone.

This year to date we have received more than 600 claims from Crombie Lockwood clients from numerous events, including storms around the country in June and July and Nelson floods in August.

This year to date we have received more than 600 claims from Crombie Lockwood clients from numerous events, including storms around the country in June and July and Nelson floods in August.

While data for this year is not yet complete, they support the upward trend in climate-related claims, as illustrated by the graph in the full report.

Online claims form introduced

Crombie Lockwood is the only insurance broker to offer an online claims lodgement capability, which enables clients to submit a claim easily, quickly and at their convenience. Clients also benefit from greater efficiency as their claims are sent directly to the insurer.

Nearly 60 percent of our SME clients are already using the online form after its introduction three months ago.

Spiralling inflation rate impacts insurance

Inflation rates continue to climb around the globe, pushed up by pandemic-related supply chain issues and the war in Ukraine. In New Zealand, annual inflation has accelerated to a 32-year high, hitting 7.3 percent for the June 2022 quarter.

However the overall CPI increase masks some areas where inflation is significantly higher than the average rate. From an insurance perspective, the construction sector is the most affected as it endures ongoing price increases and labour and material constraints. Costs for building new housing increased 18 percent in the June 2022 quarter compared to the same period last year, following on from rises of 18 percent for the March 2022 quarter and 16 percent for the December 2021 quarter. Similar cost increases also apply to the commercial building sector.

Underinsurance is a major issue in a high inflationary environment and can have substantial financial consequences in the event of a claim. The amount the insurer will typically pay for a claim is the sum insured value, which means a business will face a shortfall if the sum insured has been under stated For example, if a commercial building insured for $5 million is devastated by fire and needs to be rebuilt at the cost of $6 million, the insurer will only pay out based on the $5 million sum insured value. In such cases, the cost of the shortfall for the company is considerably greater than the additional amount needed to accurately insure the building.

Sums insured - to consider

It is imperative that all businesses review their sums insured to ensure they are adequate. With rising costs and tightening margins, many businesses are tempted to keep insurance premiums down by retaining existing sums insured. Unfortunately this approach will prove to be a false economy if a company is faced with a significant claim.

If you have any questions or want to understand the impact of these changes on your specific situation, please contact your Crombie Lockwood broker.