Hit enter to search or ESC to close

22 November 2023

Parametric insurance – a data-driven insurance solution

Parametric insurance uses data-driven solutions to provide bespoke protection from risks that are becoming more difficult and expensive to insure in a traditional way, such as natural disasters and climate-related risks.

Parametric or index-based insurance has been available for around 20 years. However, recent advances in data analytics and understanding have led to a rapid growth in availability, particularly as natural disaster (earthquake) and climate-related weather events become increasingly complex and unpredictable.

How it works

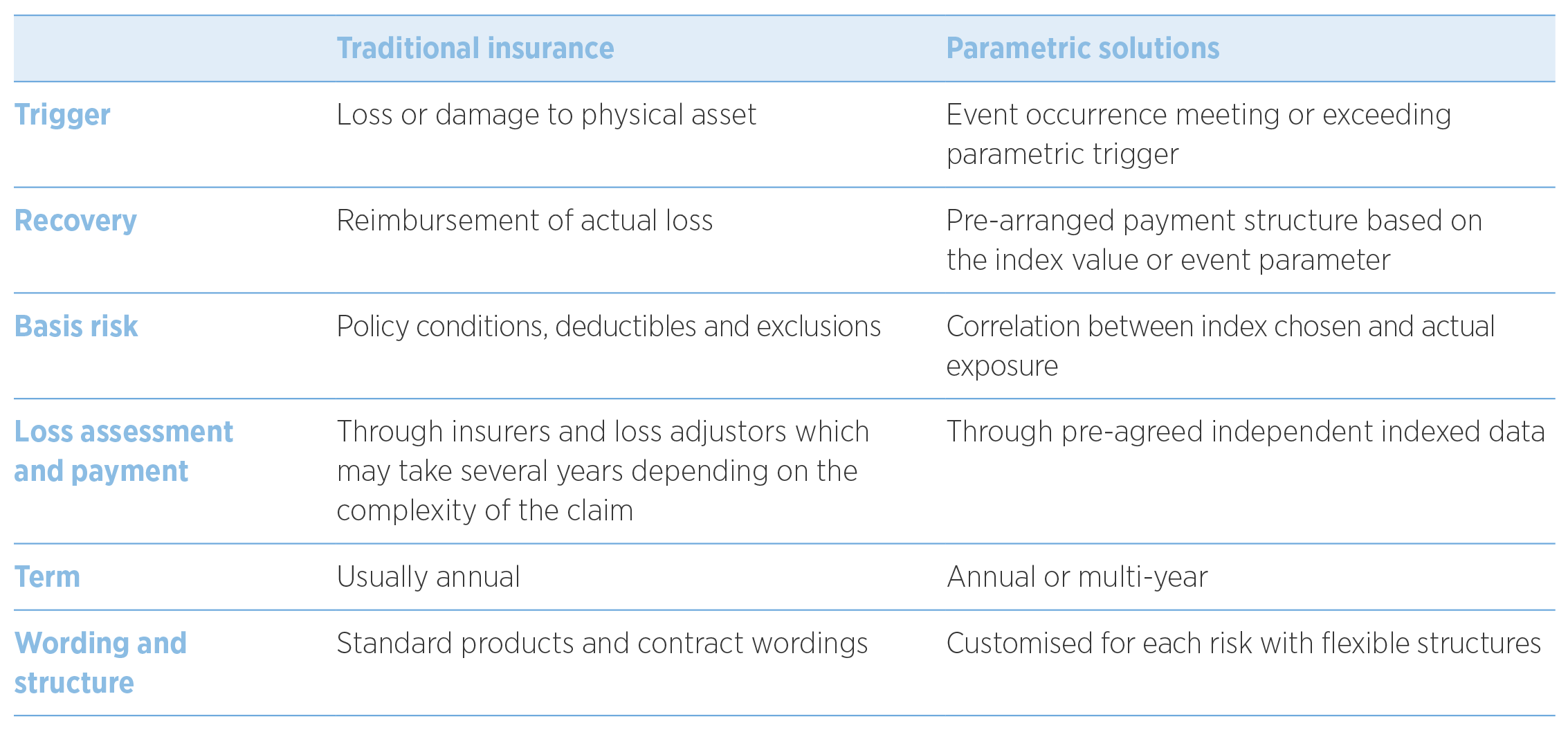

Parametric insurance provides coverage based on a pre-determined set of data, or parameters, rather than the cost of the damage caused by an event.

The policy defines how it will respond to a specific event such as an earthquake. In this case, the policy may specify that it will pay out if an earthquake of a certain magnitude occurs in a specific area – this is the policy ‘trigger’.

The insured party selects the sum insured at the outset, which does not need to relate directly to a specific asset’s value i.e. a building. The sum insured may represent additional costs that will be incurred after the event, such as loss of revenue, or it may relate to the anticipated costs of repairing damaged assets.

As a data-driven solution, the pricing of parametric insurance is based on the probability of the trigger event occurring. The insurer adds a margin to this pricing for residual risk, costs and profitability.

Parametric insurance – a snapshot

Enhanced claims experience

One of parametric insurance’s drawcards is the speed of a claims payment when trigger conditions are met. There is no need for lengthy loss adjustment and investigation as both the insurer and the insured party can rely on agreed data showing a trigger event occurred. As a result, a full pre-agreed payout can often be made within days.

Need for objective indices

With this index-based approach, it is critical that the data source used must be objective (i.e. independently verified), transparent and consistent.

Potential risks

Parametric insurance can offer a responsive and efficient alternative method to manage and transfer risk. However there are risks to using data parameters to trigger payment. With an earthquake, for example, the policy will be triggered at a certain magnitude or degree of seismic shaking at a specified location. If the earthquake does not reach the pre-defined measure of severity, no payment will be made, regardless of whether there is any actual physical damage caused.

This example highlights a key difference between traditional and parametric insurance. A traditional policy will only respond when there is actual damage to property, whereas a parametric policy will only respond if the trigger event is reached.

Specialist insurance options

There are specialist international insurers offering parametric insurance solutions for various scenarios, including:

- Earthquake – data available from GNS Science makes cover relatively easy to source for New Zealand risks.

- Flood – as traditional insurers tighten up on underwriting flood-prone risks, this area is a growing area of interest.

- Crop insurance – offers cover from damage from events such as hail, frost, rain, or even too much/too little sun

- Project delays – additional costs incurred through project delays from weather events. This can apply to construction, film and other projects.

Complements not replaces traditional insurance

Parametric solutions are designed to complement, rather than replace traditional insurance programmes. They can fill the protection gaps in indemnity insurance, such as deductibles, excluded perils, scarce capacity or pure financial risks, for example, contingent business interruption.

Understanding your natural disaster excess

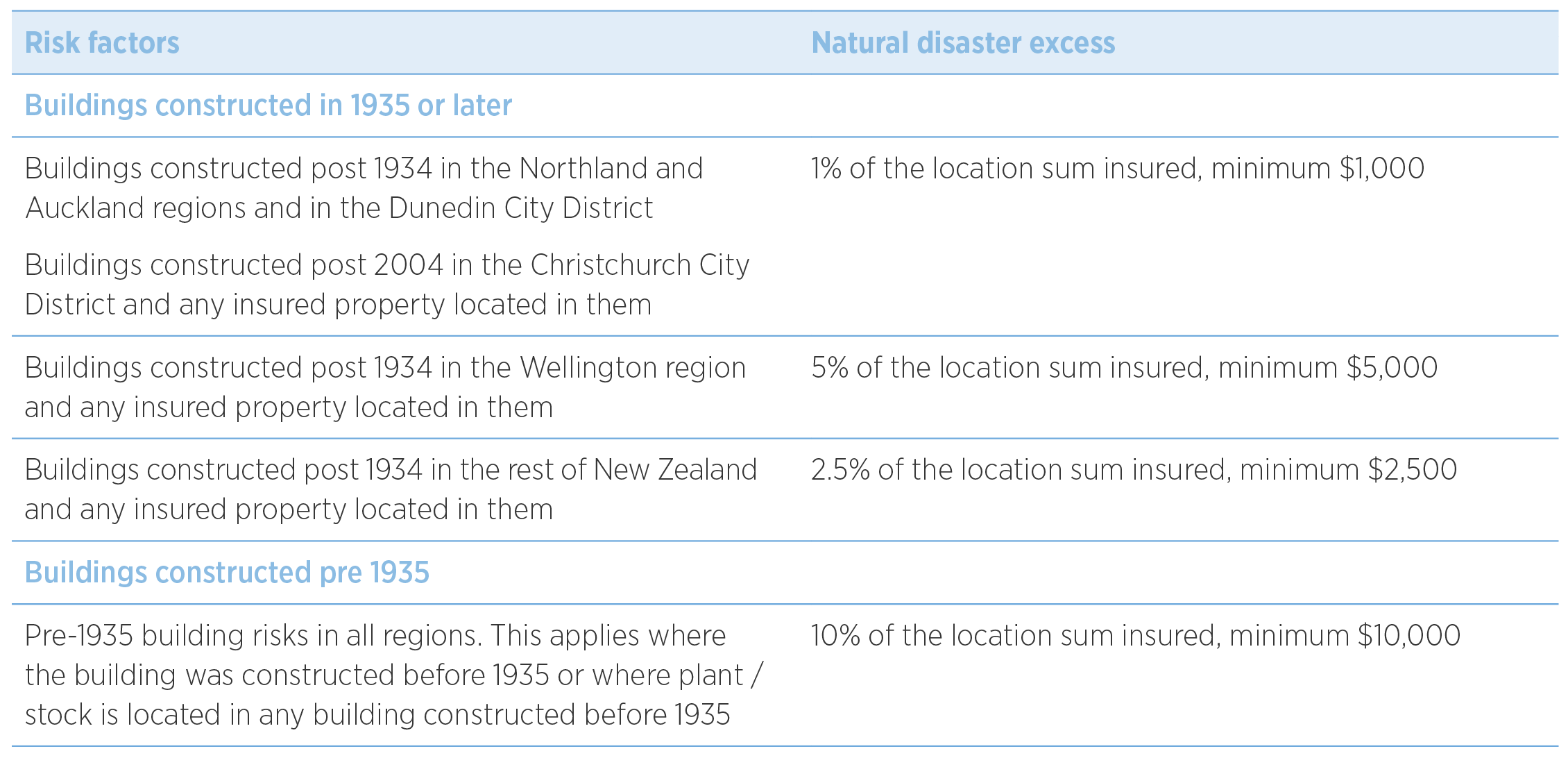

In New Zealand commercial insurance language, a natural disaster refers to the perils of earthquake, volcanic eruption, geothermal activity, hydrothermal activity, subterranean fire and tsunami. For almost all material damage and business interruption (MD/BI) policies, a natural disaster excess is based on a percentage of total sum insured (of assets) at a specific location. Although this percentage varies, it is generally based on a building’s age and the location’s exposure to earthquake risk.

Setting the natural disaster excess

The examples in the table below indicate how insurance companies set the natural disaster excess. The actual minimums and percentage applied may vary from insurer to insurer.

Understanding and funding your potential excess

It is critical to know what you may need to contribute to a claim if a natural disaster occurs. For a business with a $10 million sum insured at a single location (this includes buildings, plant and stock), the excess applicable in the event of an earthquake could range from $100,000 to $1 million, depending on the factors shown on the table on page 3. To be able to make a valid claim, the insured party needs to be able to fund the excess with available cash. This may be challenging when the amount involved is so large and failure to be able to meet the cost of the excess can prejudice the claim settlement.

Deductible Buy Down insurance is a readily available solution that provides cover for a MD/BI policy excess. It helps fund the excess when there is a claim under the MD/BI policy and also provides cover if the amount of the loss is below the MD/BI excess. (Parametric policies can also be used for this purpose).

Premiums for Deductible Buy Down insurance vary according to location and age of building.

Further information

If you have any questions or want to understand the impact of these changes on your specific situation, please contact your Gallagher broker.

For more information on issues impacting the insurance market read our November 2023 Insurance Market Update.